is this sector set to surge?

For a long time, the winning stock market sectors have been technology and anything adjacent to it. But the rise of artificial intelligence (AI) means that could be set to change.

A surge in data centre building has caused a big jump in demand for the things that go into them. And a meaningful rotation out of tech and into materials could have a huge effect on share prices.

Right now, materials companies make up around 3% of the S&P 500. That compares to around 30% for the tech sector, not including the likes of Alphabet, Amazon, and Meta Platforms.

This means cash moving from one sector to the other could have a disproportionate effect on share prices. And I think there’s a decent chance this is something we might see in the stock market.

Microsoft has a market value of $2.95trn, while Linde – the largest stock in the materials sector – is worth $236bn. That means an 8% rotation from Microsoft is enough to double Linde’s share price.

There have been signs that this kind of rotation might be starting. And if it gathers steam, then things could get really interesting across the materials sector going forward.

One way to try and profit from this might be to consider buying the iShares S&P 500 Materials Sector ETF, offering broad exposure to materials companies in the S&P 500.

The trouble is, I think some of the enthusiasm is likely to be short-lived. And it’s going to be hard for supply to react to demand falling away, which could lead to prices crashing further down the line.

In some cases though, the long-term picture looks more constructive. One example is copper, which is an important part of the shift to renewable energy, as well as data centre building. Given this, I think it’s well worth looking at some names in the copper mining space. And there’s one in particular that stands out to me.

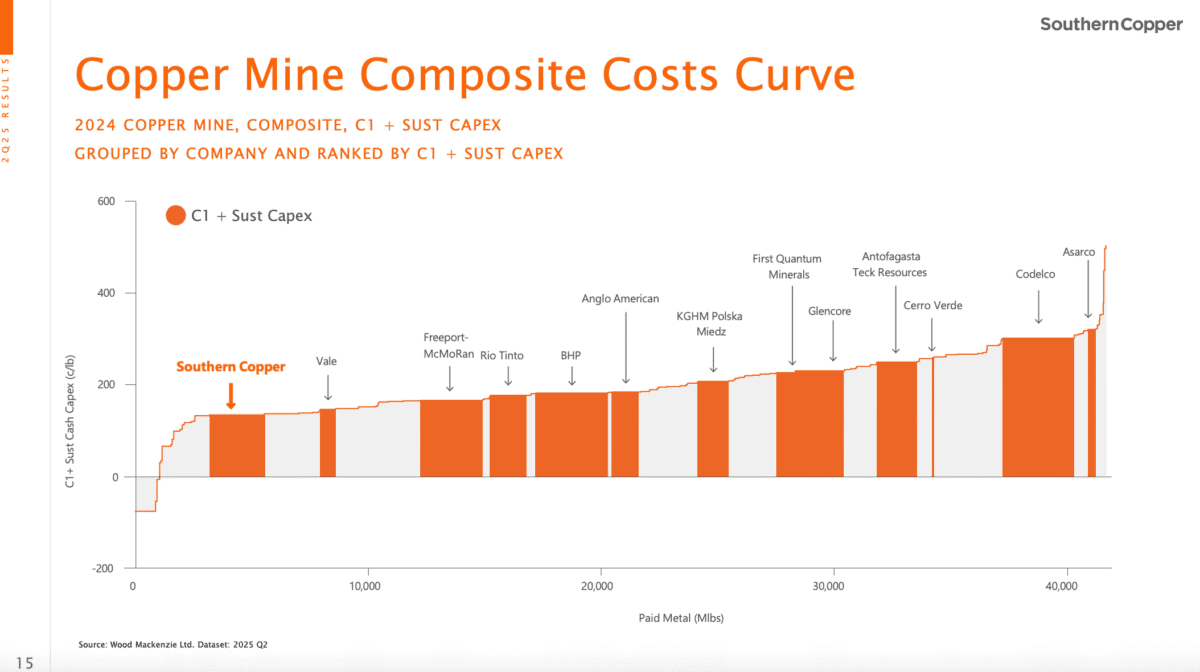

Southern Copper (NYSE:SCCO) has the largest copper reserves of any listed company and the lowest production costs. For anyone optimistic about future demand, that combination’s hard to beat.

It means there’s still significant room for things to get a lot better from this point. And it doesn’t need an earth-shattering rotation to send the stock up significantly from its current level.

The stock has been on fire over the last 12 months, climbing 145%. But the company still has a market value of around $182bn – around 6% of Microsoft’s current worth.

Source: Company Q4 2025 Presentation

The big risk is that data centre spending slows, which could cause demand to fall and prices to drop. But even if things do turn downwards, the firm’s cost-advantaged assets should still be a big advantage.

No comments

Be the first to comment.