Got $1,000? 3 Stocks to Buy Now While They’re on Sale.

A great stock is an even better buy at a lower price.

The overall market may still look overbought and feel overvalued. But a handful of stocks have actually lost some ground of late, even if they didn’t deserve to.

With that as the backdrop, here’s a rundown of three of them worth buying while you can still get them at a discount.

1. Chewy

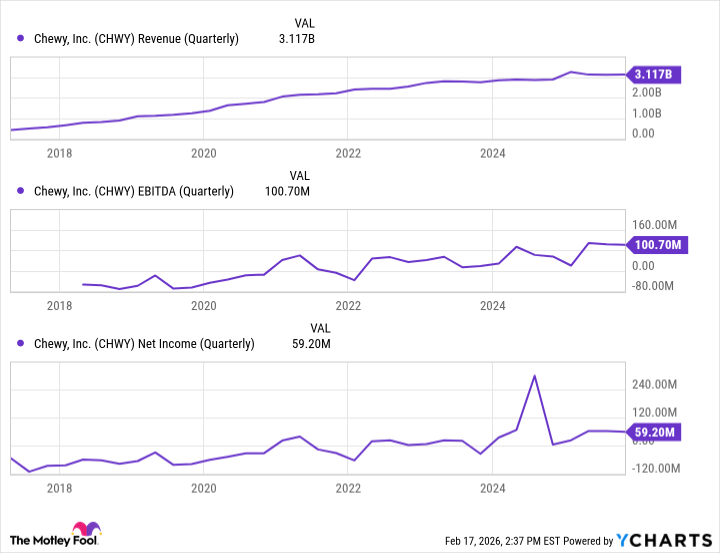

It’s been a rough past few months for Chewy (CHWY +2.34%) shareholders. Every time it looked like the stock had made a bottom, it then found a way of moving even lower. Indeed, after recently reaching yet another new 52-week low, shares of the online pet supply store and pharmacy are now priced at less than half of June’s high.

There’s still no guarantee this is a trade-worthy bottom, to be clear. It’s more likely to be one than not, however, given the underlying company’s performance of late. Last quarter’s revenue was up a little more than 8% year over year, extending a growth pace that’s been in place for years. And the company continues to grow its income after swinging to a small but sustained profit in 2022.

CHWY Revenue (Quarterly) data by YCharts

The crux of the bullish argument for owning CHWY here, however, isn’t what it’s done, but rather, how it’s done it.

See, of its fiscal third quarter’s total revenue of $3.1 billion, almost 84% of that was sales made to customers signed up for a recurring subscription to pet food, medicine, or even treats and toys. That’s up from just 80% a year earlier and markedly better than the comparison of just under 71% five years ago.

It matters simply because consumers who sign up for such subscriptions often have a “set it and forget it” frame of mind, and as such are cheaper and easier to retain as paying customers. Chewy is normalizing this e-commerce business model and ultimately enjoying widening profit margins as a result.

2. Uber Technologies

Yes, Uber Technologies (UBER +1.26%) stock tumbled earlier this month after reporting fourth-quarter profits that fell short of expectations, adding to a sell-off that’s been underway since November. All told, UBER shares are now down nearly 30% from that peak and knocking on the door of a new 52-week low.

The trading crowd’s largely misreading the situation, though. Despite missing most Q4 per-share earnings estimates with its reported profit of only $0.71 per share, that bottom line was still up 27% year over year on a 22% improvement in total trips as well as a 20% year-over-year increase in revenue. The ride-hailing company’s looking for comparable top-line growth for the quarter currently underway as well, and perhaps more importantly, expects the profit margins that were pressured last quarter to widen again, with per-share earnings projected to improve 37% year over year. Analysts, meanwhile, are calling for comparable growth for at least the next couple of years.

Image source: Getty Images.

This outlook, of course, just reflects the much bigger dynamic that Uber Technologies is plugged into. That’s consumers’ growing disinterest in driving themselves, or for that matter, even owning a car. Blame unaffordability, mostly. It’s now become cheaper to outsource personal transportation. There’s no end in sight to this dynamic either.

3. ServiceNow

Last, add ServiceNow (NOW 2.95%) to your list of growth stocks to buy while they’re on sale. This one’s down nearly 50% from its July peak.

Today’s Change

(-2.95%) $-3.17

Current Price

$104.20

Key Data Points

Market Cap

$109B

Day’s Range

$103.83 – $107.78

52wk Range

$98.00 – $211.48

Volume

679K

Avg Vol

15M

Gross Margin

77.53%

It’s not too terribly difficult to figure out why. ServiceNow is an artificial intelligence stock, and AI stocks have been sold off en masse on worries of the technology’s actual value compared to its cost.

This broad concern ignores important company-specific nuances, however, like the fact that it’s generative AI and artificial intelligence hardware companies with the most yet to prove. ServiceNow offers workplace automation solutions that provide clear, marketable value. These offerings include no-code app development, automated customer service, and digital security, just to name a few.

This practicality allows ServiceNow to turn a consistent — and consistently rising — profit. Last quarter, it turned nearly $3.6 billion in revenue into a net income of a little over $400 million, capping off a full-year bottom line of more than $1.7 billion on $13.3 billion in sales. Both were up more than 20% year over year. Analysts are looking for comparable growth this year and next too, despite the apparent slowdown other AI companies seem to be facing.

Most investors appear to have lost sight of how well this company is positioned to continue thriving for the foreseeable future even if other names in the AI business don’t. The analyst community hasn’t, though. In addition to most of them still rating NOW as a strong buy, its consensus price target is holding strong at $187.69, up 78% from the stock’s current price. Once investors are reminded that the nature of ServiceNow’s business shields it from more sweeping headwinds, don’t be surprised to see this stock start moving back toward that target.

No comments

Be the first to comment.